BIG DISCLAIMER: Sponsored Content with Endowus, a roboadvisor. You can check them out here, or sign up with them here. Of course, you should read this article before you come to a decision. If your needs are complex, a roboadvisor might not be the best choice for you.

****

Our audience has been asking two questions:

- How to pick a robo-advisor?

- Whether or not investing through a financial advisor is okay?

Turns out, these questions are pretty much asking the same thing: Who should manage your money?

And turns out, both human and financial advisors have many similarities.

So we’ve merged these two topics into one. And then we got Endowus to pay for it (genius, I know).

Whether or not you choose a human advisor or a robo-advisor, here are some very important questions you should ask to make sure you are in good hands.

#1 What is their track record?

Here’s how we would do a background check on verifying a good human advisor.

- Ask how long they’ve been in the industry. Some advisors promise to service your policies long-term, but then stay in the industry only for a year. Pick someone who’s serious about this as a career.

- What people say about them. Ask for references from past clients, but also look out for alternative sources of recommendations (mutual friends, forums, Googling.)

- Asking for an investment track record might be difficult if you’re working with a younger financial advisor. But you can ask for the track record of the funds they intend to buy for you.

- How they carry themselves. You might have guessed this already, but we’re not fans of financial advisors flexing nice watches and cars, accompanied by pressure sales tactics.

(I’m sure they have their market). We’d look for financial advisors who are more aligned with our values.

For robo-advisors, the process is simpler, and there are four ways you can check:

- You can read reviews of them online on places such as Seedly, MoneySmart or ValueChampion, and even how their fund performances stack up against one another.

- Following a whole bunch of credible financial bloggers will also help.

- Yes, Endowus paid us for this sponsored post, but you can be damn sure we won’t risk our reputation just to earn a quick buck. A bad reputation affects our long-term ability to make money.

- Stalking the bio of the team members. Who is their CIO (Chief Investment Officer)? They should have significant experience in the finance industry. Expertise matters, right? Otherwise what are you paying for?

#2 How responsive are they?

You buy an investment plan from a financial advisor, and that’s the last time you ever hear from them again. Even when you ask them for investment advice.

Until of course, you cancel that plan – which will trigger a whole song and dance from said advisor.

Sounds familiar?

Well, unfortunately we’ve heard that story one too many times.

Okay, look.

Not to shit on human advisors, because there are great ones out there who really know their stuff and constantly update their clients on their portfolio performance.

But you need to be really careful when you pick one, because the range of service you get from one is so wide. Your advisor could be catatonic or super responsive. And you only find out after you’ve committed yourself to a plan.

Here’s our take – you pay advisors “an advisory fee” – so they are at least supposed to advise you regularly.

That means at the very least, they should check in with you for reviews (without the intention to upsell indiscriminately).

Whereas for a robo-advisor, you can get updates via a platform that’s accessible for everyone.

TBH we haven’t tried contacting our robo-advisor for customer service before – but with a transparent platform, we never really saw a need to anyway.

#3 How do they make money?

Knowing how anyone makes money is really important, because it offers clues to find out whether or not they act in your best interest.

Most advisors – robo or humans – make money like this:

- You (via advisory fee)

- Commissions from the funds that they sell you (trailer fee)

The latter is somewhat controversial as it might lead to a conflict of interest.

For example, if the advisor makes more money from commissions instead of advising you – they might not always act in your interest.

We want to stress this doesn’t mean that trailer fees/commissions = bad. There are plenty of great commission-earning financial advisors. But it can be one of the factors you put into consideration when considering your advisor.

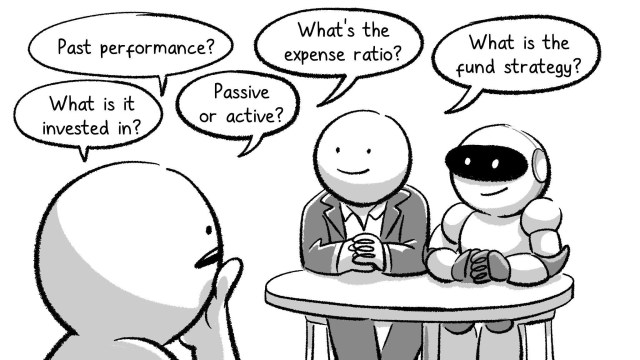

#4 What are they selling you, and just how much do they know?

Human or robo, it is useful to know what specific funds your money is invested in, as well as the advisor’s rationale behind picking the fund (see previous point).

Some questions you might want to ask include:

- How much are the fund’s expense ratios, and if they are higher-than-normal, why are they justified? (Fund fees generally range from 0.5 – 1.5%)

- How has this fund performed for the past 3, 5, 10 or even 15 years?

- What is the aim of this fund? Is it for growth, defensive or for income?

- What is this fund invested in?

- Is it passively or actively managed? And what are the advantages of both?

For example:

A financial advisor might tell you they invested in the FSSA Dividend Advantage Fund for you, and they could tell you that…

It has consistently outperformed its benchmarks over the past 10 years, has an experienced management team, and is exposed to emerging markets in Asia, as well as Japan and Australia.

If someone tells you ‘aiya don’t ask so much, just trust me’, then it’s a major red flag.

#5 Human or robo-advisor?

Look, even though this post is sponsored by Endowus, doesn’t mean that you can’t get the job done via a human advisor.

IMHO, a robo-advisor would be more suitable for some who have simple financial needs and are just looking for the absolute cheapest way to invest.

When you don’t have a lot of money, you don’t need someone to customise investment plans for you.

The more complex your financial situation is, then more likely you’ll need a human advisor.

The main selling point of a human advisor is that they are supposed to do more than just investments – but also advise you on insurance, estate-planning, tax, debts, as well as other investment classes, such as property.

For example – if you’re a 55-year-old multi-millionaire business-owner who has two families you need to insure, invest and do estate-planning for…then you probably appreciate a human advisor.

Just for the lulz, here’s a helpful table for your kind perusal:

Table 1.1

An exhaustive list of key differences between a robo-advisor and a human advisor

| Robo-advisor | Human advisor |

| Less customisation; pick from an array of pre-set portfolios | More customisation |

| Mostly deals with investments | Has a wider range of services, including estate planning and insurance |

| Doesn’t wear Hermes Belt and drive BMWs | Might wear Hermes Belt and drive BMWs |

| Generally lower fees because of economies of scale and network effects | Generally higher fees, because more customisation |

Passive investing doesn’t mean passive financial planning

Passive investing via robo-advisors is pitched as a magic bullet to all your financial problems these days. This is only half true.

Yes, it’s simple and relatively uncomplicated. But it’s also important to realise that being a passive investor means you do less, but not NO due diligence.

Our take? Set aside one day and sit down, then go through the options before you make a decision.

Your approach to investing can be passive.

But your approach to your money can’t be.

Stay woke, salaryman.

A message from our sponsor, Endowus.

We’ve been using Endowus since 2019, and we’ve found using it to be pretty smooth and intuitive.

Some advantages over the other robos include:

#1 Only platform that you can invest ALL your money

Many robos let you invest your money conveniently, but Endowus is the only platform that allows you to conveniently invest not only Cash but CPF and SRS in one platform.

That means you have the option of investing your CPF in passive, low-cost Vanguard funds.

The starting minimum is now also $1,000 (used to be $10,000).

#2 Wide access to highly-rated, low-cost funds

They are also the only robo that allows you to pick and choose a portfolio of funds (called “Endowus Fund Smart”), just like how you can get a financial advisor to tweak your portfolio. They don’t do estate planning tho. You still need a human advisor for that.

#3 Transparency over what you’re charged (see below)

Endowus is so transparent with what they invest in, you could technically try to replicate their portfolio on your own. But brokerage fees and FX costs might make that inefficient if you were to DIY invest.

Create an Endowus account using this link and get $20 off your access fee across your CPF, SRS and Cash investments.

The fact u labelled one of the difference between robo and human is having hermes and driving bmw proves how dense and desperate representatives of endowus are.